Key headlines

Analysing M&A and capital markets data from the Real Estate industry, we share our experience of trends that have emerged following COVID-19.

Source: Data from IVBL (January 2021)

2020 saw a 25% year–on-year decline in deal values, and a 44% decline in deal volumes. The impact of the pandemic after April 2020 was stark. By deal value Q1-20 started well, representing more than double Q1-19, but once COVID-19 hit, deal volumes fell by 61% and values more than halved (a 52% fall), comparing April to December year-on-year. We did, however, see an uptick towards the end of the year with September and October deal values ahead of 2019. BDO in fact observed a busy spurt in the run up to Christmas.

A number of overarching trends emerged out of COVID-19:

Sector update – M&A transaction values and weighted average transaction yields (see note)

![]()

Note – yield data for a period reflects the average yields from all transactions in that period where yield data is available

Since the summer, many speculated that hikes to capital gains tax rates were coming, initially in the Autumn Statement and more recently the Spring Budget, which has driven a surge in private business sales in the latter half of 2020 (continuing into this year). This is not unique to the real estate industry, and has underpinned certain decision making and exit planning by business owners across the UK (Read more here). A report on CGT reform by the Office of Tax Simplification was published on 11 November 2020 which further stoked the speculation by recommending closer alignment of income tax and capital gains tax rates (Read our review of the proposals). However, the nature and timing of any changes remain uncertain and may still be influenced by economic indicators as government monitors the impact of the pandemic.

A move towards ‘sheds, breads, beds or meds’. Industrial, supermarket, residential, and healthcare M&A held up comparably well where rent collections have been strongest and investments are seen as more future proof. In the main, average yields tightened year-on-year and deal activity continued throughout 2020.

Retail, student and leisure unsurprisingly hardest hit. Student and hotel M&A largely dried up, and whilst there were shopping centre and high street deals, they substantially reflected large investors divesting out of these sectors and rebalancing portfolios, often selling abroad.

There is still appetite for offices and business parks, albeit M&A has been selective. Yields compressed on average (bolstered by comparably positive rent collections) whilst deal volumes were down. There have been signs of town offices becoming more desirable, and investors are telling us they have now very different requirements from office space, with mixed usage and the ability to change/develop the property important factors.

Deals by investor type

Overseas investors contributed over half of the investment in 2020, with our overseas clients telling us that the UK still seen as desirable and a target market (perhaps also buoyed by the relatively weakened Pound).

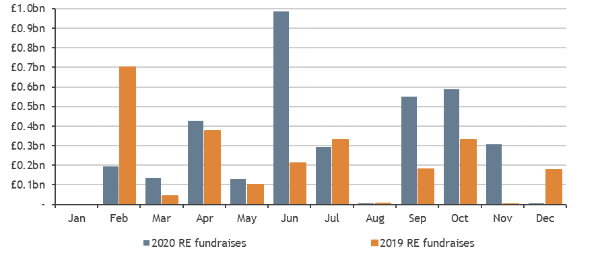

REITs and private propcos were hardest hit investors year-on-year, albeit REITs became more active towards the end of 2020. Many listed REITs found their share prices heavily discounted to their net asset value as COVID-19 drove 40%+ falls in AIM and the FTSE. This limited their ability to raise equity and complete transactions over the summer. Meanwhile, PLCs in the hardest hit sectors tapped the markets for emergency funding to shore up balance sheets, making 2020 the busiest year for capital markets fundraises in the last decade.

AIM and – to a lesser extent - the FTSE have since gradually recovered (AIM now sits higher than pre COVID levels), and as a result REITs in the more buoyant sub sectors (in particular industrial, supermarket, residential, and healthcare) have since seen their discounts to NAV unwind. These REITs were able to raise equity (and debt, as banks’ confidence has since grown) between September and November 2020 to then deploy in transactions. While not necessarily a sustained return to pre COVID-19 levels, we expect a continuation of this trend into Q1-21.

Listed real estate equity fundraises (AIM and Main Market) in 2020 and 2019

Source: LSA Data

London was the least affected region, falling by 20% year on year, but all regions were significantly impacted (see [below]). ‘Portfolio’ deals remained stable year on year, and so increased their market share to 32% (up from 25%). Much of this was driven by the £4.7bn student portfolio investment made by Blackstone in Feb-20.

Regional transactions mix by value – 2019 (inner) vs 2020 (outer)

.png)

![]()

Source: LSA Data

Outlook

The resurgent M&A activity towards the end of 2020 was encouraging, and we are already seeing this trend continuing into 2021. Equity markets are very much open and the availability of debt appears to be improving.

The prospect of low interest rates in the short-to-medium term has also made listed REITs and real estate in general relatively more desirable investments for those seeking a yield-based return. However, investors continue to be selective, and we expect investment to remain skewed towards sub-sectors with more stable tenants and higher rent collections, notably logistics, healthcare, supermarkets, residential and offices. Meanwhile, as UK lockdown measures endure, large real estate investors are telling us their strategies remain geared towards divesting their portfolios away from retail and leisure assets. Overseas funds are no doubt waiting in the wings to pick up a bargain.

As for the slightly longer term, COVID-19 has accelerated change in the real estate sector. It is clear that remote and flexible working is here to stay, with many businesses sharing that employees plan to work from home at least twice a week. The office sector and wider real estate market needs to shift to cater for this change, and we could see transformational changes to our high streets and city centres.

ESG is also much more prominent in the mindset of real estate investors. 2020 saw a surge in renewables activity which has crossed over into the real estate sector - Tritax BigBox Plc raised a £250m green bond before Christmas - and a number of social impact funds have emerged, including Home REIT Plc, which was set up to invest in homeless shelters across the UK. The focus on ESG appears to be one of the true silver linings emerging out of COVID-19 that will shape the future of the sector.

Real Estate was BDO's most active sector, by value, to find out more visit our Corporate Finance hub.

Subscribe to receive the latest BDO News and Insights

Please fill out the following form to access the download.